When people discuss embedded finance, the conversation typically revolves around fintechs, neobanks, and other digital-native players. But that view is quickly becoming outdated.

Today, companies in retail, lending, logistics, payroll, and travel are embedding financial services, not to become banks, but to take control of customer experience, reduce operational friction, and unlock new revenue streams. And one of the most powerful tools enabling this shift? Embedded card issuing.

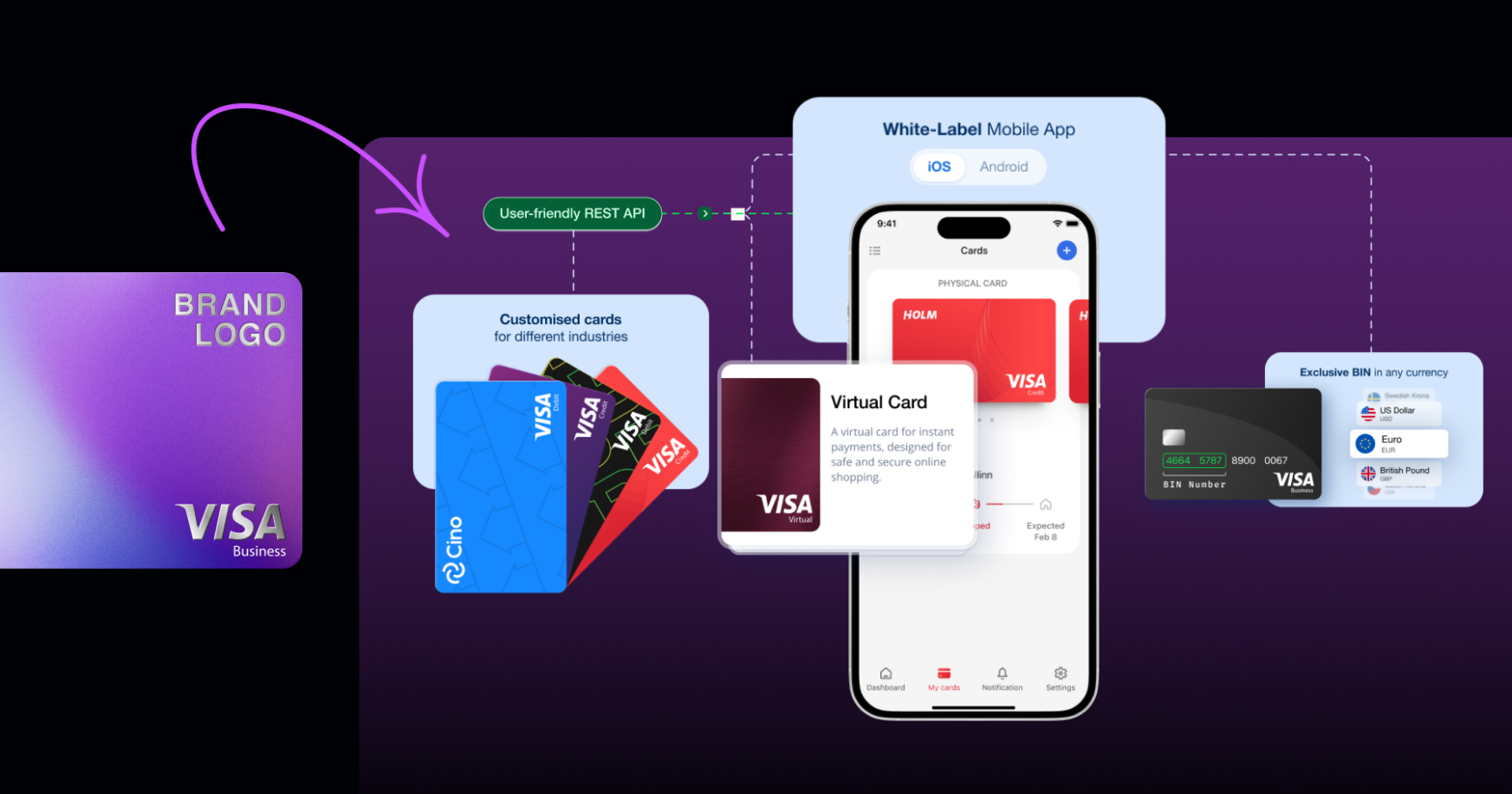

With Cards-as-a-Service platforms like Wallester White-Label, any company can launch its own branded payment cards, virtual or physical, without needing a banking license or building infrastructure from scratch.

Let’s break down what this means in real terms and why embedded card infrastructure is no longer just for fintechs.

What Is Embedded Finance, Really?

Embedded finance refers to the integration of financial services directly into non-financial platforms. Instead of redirecting users to external banks or payment providers, companies bring financial functionality, like payments, lending, or insurance, into their own products.

In the case of embedded cards, this means businesses can issue and manage branded payment cards, integrate them into their workflows or products, and retain full control of how payments happen.

The old way? Rely on traditional providers and institutions to control customer payments.

The new way? Issue your own cards, own the data, own the experience.

Why This Matters Beyond Fintech

You don’t need to be a bank to benefit from embedded cards. Any business that moves money to customers, vendors, employees, or partners can take advantage. Here’s why more companies outside of traditional finance are embedding card infrastructure:

- Customer experience: Offer potentially faster payouts, easier access to funds, and seamless transactions, all under your brand.

- Revenue growth: Generate revenue through interchange fees and cardholder activity.

- Operational control: Set spending rules, automate reconciliation, and monitor transactions in real time.

- Brand visibility: Put your brand in your customer’s wallet or phone, not the bank’s.

- Speed to market: With white-label platforms, companies can go live in weeks, not years.

Real-World Examples Across Industries

Let’s explore how embedded cards are transforming industries far beyond fintech:

1. E-Commerce & Marketplaces

Use case: Branded payout cards for sellers.

Why it works: Skip manual bank transfers and delays. Let vendors access their funds instantly, and incentivise platform loyalty through branded reward cards or cashback.

Example: A marketplace issues cards to thousands of sellers, boosting retention and unlocking new margins from card activity.

2. Loan Providers & Buy-Now-Pay-Later Platforms

Use case: Instant loan disbursement via virtual or physical cards.

Why it works: Customers don’t want to wait for funds. With cards, loans can be accessed and used immediately, even added to Apple Pay or Google Pay within seconds.

Example: A digital lender embeds cards into its app to streamline distribution, increase usage, and eliminate reliance on slow bank rails.

3. Gig Platforms

Use case: On-demand pay cards for freelancers, contractors, and shift workers.

Why it works: Workers can get paid instantly after each job. No more waiting for bank transfers or managing cash.

Example: A gig platform uses branded payroll cards to reduce churn and stand out from competitors. They can also implement a cashback system, sharing interchange fees, to create added loyalty.

4. Travel & Mobility Services

Use case: Expense cards for drivers, couriers, or staff on the move.

Why it works: Set daily spend limits, manage fuel or lodging costs, and gain full visibility across the fleet, all from one platform.

Example: A tour operator replaces petty cash and manual reimbursements with real-time controlled spending cards.

5. B2B Services & Procurement

Use case: Corporate payment cards for departmental budgets, client expenses, or supplier payments.

Why it works: Improve financial control, reduce fraud, and eliminate time-consuming invoice processes.

Example: A procurement firm offers clients branded cards to manage purchases directly, adding value and monetising usage.

The Infrastructure Shift: You Don’t Need to Build It Yourself

Until recently, launching your own card program meant becoming an issuer, hiring compliance teams, and handling everything from KYC to fraud monitoring. It was prohibitively complex and expensive.

Platforms like Wallester White-Label remove those barriers. We provide:

- Instant virtual and physical card issuing (with Visa connectivity)

- Custom branding, your logo, your card design

- Full BIN sponsorship and licensing

- Real-time expense controls and transaction monitoring

- API-driven integration with your existing systems

- AML, KYC, fraud detection, and compliance infrastructure built in

In short, you get the power of a full-scale card-issuing bank, without needing to become one.

Why Now?

Three key forces are accelerating embedded finance:

- Customer expectations: Speed, flexibility, and digital-first experiences are now the default.

- Competitive pressure: Embedded financial features create real differentiation in crowded markets.

- Access to infrastructure: Thanks to API-first platforms, what once took years now takes weeks.

If you’re still outsourcing the customer experience to banks, you’re leaving value on the table.

Conclusion: Embedded Finance Is About Creating Value

Embedded cards are no longer the exclusive domain of fintechs. Whether you’re running a gig economy platform, a B2B marketplace, or a travel business, issuing your own branded cards puts you in control.

You create smoother customer journeys.

You build brand loyalty.

You unlock new revenue streams.

And with the right partner, you don’t need to build it all yourself.

Wallester White-Label enables businesses of all kinds to embed financial services at speed and scale, securely, compliantly, and under your own brand.

If you’re moving money, it’s time to move smarter.