When you pull out your credit card to make a purchase, you see different logos on it – perhaps Visa or Mastercard on one side, and your bank’s name on the other. The logos represent two distinct entities that work together to make your transactions possible: the credit card network and the card issuer. Knowing how they differ can help you understand how your card works – and why some offer different terms, benefits, or acceptance levels.

Key takeaways

- Networks like Visa and Mastercard establish the infrastructure for processing payments but don’t issue credit cards directly to consumers.

- Card issuers are financial institutions that approve applications, set limits, and collect payments from cardholders.

- Major networks include Visa, Mastercard, American Express, and Discover.

- Some companies like American Express and Discover function as both a network and an issuer (closed credit card networks).

- Networks charge various types of fees, including interchange, assessment, and processing fees.

- Card issuers determine interest rates, rewards programmes, and customer service offerings.

What is a credit card network?

A credit card network acts as the core infrastructure that makes payments possible. These networks function as virtual infrastructures connecting merchants, customers, and financial institutions. When you swipe, tap, or insert your card at checkout, the network facilitates the process by securely transmitting payment information between the involved parties.

Networks establish rules for how payment card transactions flow and set standards for security. They don’t interact directly with consumers by issuing cards or setting credit limits. Instead, they maintain the systems that allow money to move securely between accounts when purchases occur.

Major networks possess global reach, allowing cardholders to make purchases almost anywhere. These companies earn revenue mainly through fees charged to merchants and financial institutions. The four major networks dominating the market today are Visa, Mastercard, American Express, and Discover, although the latter two operate somewhat differently.

Why are credit card networks important for businesses?

Networks play a very important role for merchants of all sizes. By connecting to these systems, businesses can accept payments from customers carrying cards issued by countless banks and credit unions, vastly expanding their potential customer base.

The infrastructure provided by networks protects businesses through sophisticated security measures. When disputes arise, standardised procedures help merchants handle cardholder issues consistently.

For global businesses, networks offer the advantage of standardised processing across different countries and currencies. This allows companies to expand internationally without building separate payment systems for each market. The rapid processing offered by modern networks also means businesses receive funds quickly, aiding cash flow.

Key benefits of credit card networks for businesses:

- Global acceptance and currency handling.

- Fraud protection and security standards.

- Fast settlement and cash flow improvements.

- Dispute resolution frameworks.

Further Reading: The Best Corporate Cards in the UK for 2025

Types of card networks

Credit card networks generally fall into two categories: open and closed networks.

- Open networks, like Visa and Mastercard, focus solely on processing rather than issuing cards directly. They partner with financial institutions worldwide that distribute cards to customers. These issuers decide on applications, credit limits, and account terms. Open networks primarily generate revenue from transaction processing fees.

- Closed networks, like American Express and Discover, function both as networks and issuers. They handle processing while also issuing cards directly to consumers. This gives them greater control over the customer relationship and the entire payment chain. Historically, closed networks have targeted higher-income consumers and charged merchants higher acceptance fees, although the gap has narrowed over time.

Some operate hybrid models. For example, American Express, while primarily closed, partners with banks in some markets to issue branded cards, creating a partially open structure.

Card networks examples

The industry features several major credit card networks, each with distinct characteristics.

Visa stands as the largest, processing billions of transactions annually across more than 200 countries. Known for universal acceptance, Visa partners with thousands of banks and credit unions, never issuing cards directly.

Mastercard operates similarly to Visa, providing processing infrastructure while partner banks issue the cards. Mastercard enjoys comparable global acceptance and is recognised by its interlocking red and yellow circles.

American Express primarily operates as a closed network, acting as both processor and issuer. Known for targeting premium customers, Amex cards typically offer extensive rewards but have historically faced limited acceptance due to higher merchant fees. Acceptance has broadened significantly in recent years.

Discover also functions as both network and issuer in the U.S. Originating from Sears in the 1980s, Discover has expanded its global reach through partnerships but remains more U.S.-centric compared to Visa and Mastercard.

Other examples include China UnionPay, dominant in China, and JCB from Japan, which has expanded throughout Asia and beyond.

Fees charged by credit card networks

The networks implement several types of fees that affect various parties in the transaction process. These fees help explain how networks generate revenue.

Three main types of fees apply to most transactions:

- Interchange fees – The largest component (1-3% of transaction value), paid to the financial institution that issued the card

- Assessment fees – Smaller fees (0.1-0.15%) paid directly to the payment network for using their infrastructure

- Processing fees – Technical costs for moving transaction data securely between parties

Additional factors affecting fees include:

- Transaction type (in-person vs. online)

- Business category (restaurants, retail, etc.)

- Card type (rewards cards typically cost merchants more)

- International transactions (which incur additional cross-border transaction fees)

Merchants often face higher fees when accepting premium reward cards that offer significant benefits to cardholders. It creates tension in the industry, as these premium cards are attractive to consumers but more costly for businesses to accept. In some regions, regulations have been implemented to cap interchange fees, particularly for debit card transactions.

Is there a difference between card networks?

While networks perform similar core functions, notable differences exist.

Acceptance rates vary. Visa and Mastercard enjoy near-universal global acceptance. American Express and Discover have high acceptance in the United States but can face limited reach internationally or among smaller merchants.

Security features differ as well. Visa uses Visa Advanced Authorisation, while Mastercard offers SecureCode. These backend systems vary in sophistication but work to protect transactions.

Fee structures are another point of differentiation. American Express traditionally charges higher merchant fees than Visa or Mastercard, influencing where these cards are accepted.

Each network offers specialised services. American Express provides detailed consumer spending insights, while Visa offers comprehensive fraud management tools.

Dispute resolution processes also differ slightly, affecting how quickly and favourably consumer disputes are handled.

Key differences among networks:

- Global acceptance rates.

- Merchant fee structures.

- Fraud protection technologies.

- Consumer and business services.

- Dispute resolution procedures.

Do credit card networks offer rewards?

Networks themselves usually don’t directly offer rewards to consumers. Instead, they create frameworks that issuers use to structure reward programmes. Card issuers design and fund specific rewards offerings. Whether you earn cashback or travel points, the issuer – not the network – funds those incentives.

However, networks provide standardised benefits across their cards. Visa tiers benefits into Classic, Signature, and Infinite levels, offering features like purchase protection and travel assistance. Mastercard provides Standard, World, and World Elite packages.

American Express and Discover act as both network and issuer. They control their reward offerings more directly, integrating them tightly with their processing and customer relationship strategies.

What is a credit card issuer?

A card issuer is a financial institution that provides cards directly to consumers. Issuers manage customer accounts, make credit decisions, and fund cardholder purchases. They review applications, approve or deny based on creditworthiness, and set individual credit limits. Issuers also determine interest rates, annual fees, and reward structures.

When you use a credit card, the issuer is effectively lending you money for your purchases. Issuers also handle customer service, dispute management, and card replacements. Examples of issuers include large banks like Chase, Citi, and Bank of America, specialised card companies like Capital One and Discover, and even some credit unions and retailers.

Card issuers examples

The market includes a wide range of issuers, each offering distinct advantages.

- JPMorgan Chase is the largest U.S. issuer by purchase volume. Products like the Chase Sapphire Preferred, running on the Visa network, are popular among travellers seeking rewards.

- Citibank operates globally across multiple networks. The Citi Double Cash Mastercard is noted for its straightforward cashback structure, while Citi’s relationship with American Airlines provides robust co-branded travel options.

- Bank of America offers cards focused on cashback and relationship rewards, with programmes like Preferred Rewards enhancing benefits for customers with larger deposits.

- Capital Onehas grown into a top issuer, known for flexible rewards cards like Venture and Quicksilver, often favoured by consumers valuing simplicity.

- American Express operates as both network and issuer, offering premium products like the Gold and Platinum Cards, known for luxury travel benefits.

- Discover, similarly dual-role, is recognised for its consumer-friendly rewards model, including cashback match promotions for new users.

Credit unions often issue cards as well, promoting lower interest rates and favourable terms compared to traditional banks.

Further Reading: Top 10 Credit Cards in Germany in 2025

How do credit card networks and issuers differ?

Understanding the distinct roles of credit card networks and issuers clarifies the structure behind every transaction. Their different functions complement each other in making the payment system work smoothly.

Card issuers maintain direct relationships with cardholders. They approve applications, set credit limits, and collect payments. Credit card networks, conversely, rarely interact directly with consumers, instead focusing on the infrastructure that connects merchants, banks, and customers.

Regarding fees, issuers primarily earn revenue through interest charges, annual fees, and their portion of interchange fees. Networks generate income mainly through assessment fees charged to banks and payment processors for using their systems. The issuer extends credit to consumers, effectively lending money when purchases are made. Networks don’t lend money; they simply facilitate the secure transfer of transaction information.

When problems arise, cardholders contact their issuer for account issues like billing disputes or payment questions. Networks typically become involved only for systemic issues affecting the payment infrastructure. Card issuers handle services like card replacement, credit limit increases, and rewards redemption. Networks focus on maintaining the technological systems that allow transactions to flow securely.

The issuer makes the final decision on whether to approve specific transactions based on available credit and fraud indicators. Networks provide the pathways through which approval requests travel but don’t make those decisions themselves. Issuers offer customer protections like zero liability for fraud, while networks establish broader rules and standards for security across their systems.

Networks and issuers: how they work together

Networks and issuers work in tandem to complete each transaction.

When you make a purchase:

- The merchant’s bank (acquirer) submits a transaction request through the appropriate network.

- The network routes the request to the card issuer.

- The issuer checks your account for available credit and signs off or denies the transaction.

- Approval is returned through the network to the merchant.

The settlement follows as the acquirer pays the merchant, seeking reimbursement from the issuer, who in turn bills the cardholder. Throughout this flow, various fees are collected.

In cases of cardholder disputes, issuers initiate the chargeback process, which proceeds through the network according to established rules. Each party’s role ensures that purchases are processed quickly, securely, and fairly.

What is the best credit card network and issuer for you?

Choosing the optimal combination of credit card network and issuer depends on your spending habits, travel patterns, and financial goals. Several factors deserve consideration before making your choice.

For frequent international travellers, cards on the Visa or Mastercard networks usually offer the widest global acceptance. These networks function in almost every country. It makes them reliable choices for worldwide use. American Express and Discover have expanded their international presence but still face more limited acceptance in some regions.

Consider how you plan to use your card most frequently. If you are looking for everyday domestic spending, any of the four major networks provides sufficient coverage in the United States. However, if you frequently visit small, independent businesses, Visa and Mastercard have better acceptance rates due to their lower merchant fees.

Regarding issuers, examine the various rewards programmes offered. Some issuers excel at cashback programmes, while others focus on travel rewards or points systems. Match the issuer’s specialty to your spending priorities for maximum benefit. Also compare interest rates if you occasionally carry a balance, as rates can vary significantly between issuers even for customers with similar credit profiles.

Customer service quality differs among issuers, with some offering 24/7 phone support, reliable mobile apps, and quick response times. Others might provide more limited access or slower response to issues. Annual fees represent another important consideration, as premium cards can charge $500+ yearly while many quality options charge no annual fee.

For business owners, different networks and issuers offer varying tools for expense management and accounting integration. Business credit cards from specialised issuers might include features like employee cards with custom spending limits or detailed categorisation of expenses.

Further Reading: Virtual Cards vs. Physical Cards: What’s Better for Business?

Conclusion

The distinction between credit card networks and issuers plays a fundamental role in how credit card transactions function. Networks like Visa and Mastercard provide the essential infrastructure that allows payments to flow between customers, merchants, and financial institutions. Issuers such as Chase, Bank of America, and Capital One handle the direct customer relationships, determining who receives credit and under what terms.

Understanding this division helps explain why your card displays two different company logos and clarifies who to contact for different types of issues. When experiencing billing problems or reward questions, your issuer serves as the proper contact. For acceptance issues at merchants, the network typically bears more responsibility.

The credit card industry continues growing with technological advancements and changing consumer preferences. Contactless payments, mobile wallets, and stronger security features are among the key innovations changing the way we use credit cards. Both networks and issuers adapt to these changes but continue to perform their core roles in the payment system.

The complex fee structure between merchants, networks, and issuers funds the convenience of credit card payments. Although these relationships can sometimes create tension between parties, they still allow transactions to be processed smoothly – just as consumers have come to expect. As payment technologies continue advancing, the fundamental relationship between networks and issuers will likely remain at the heart of the credit card industry.

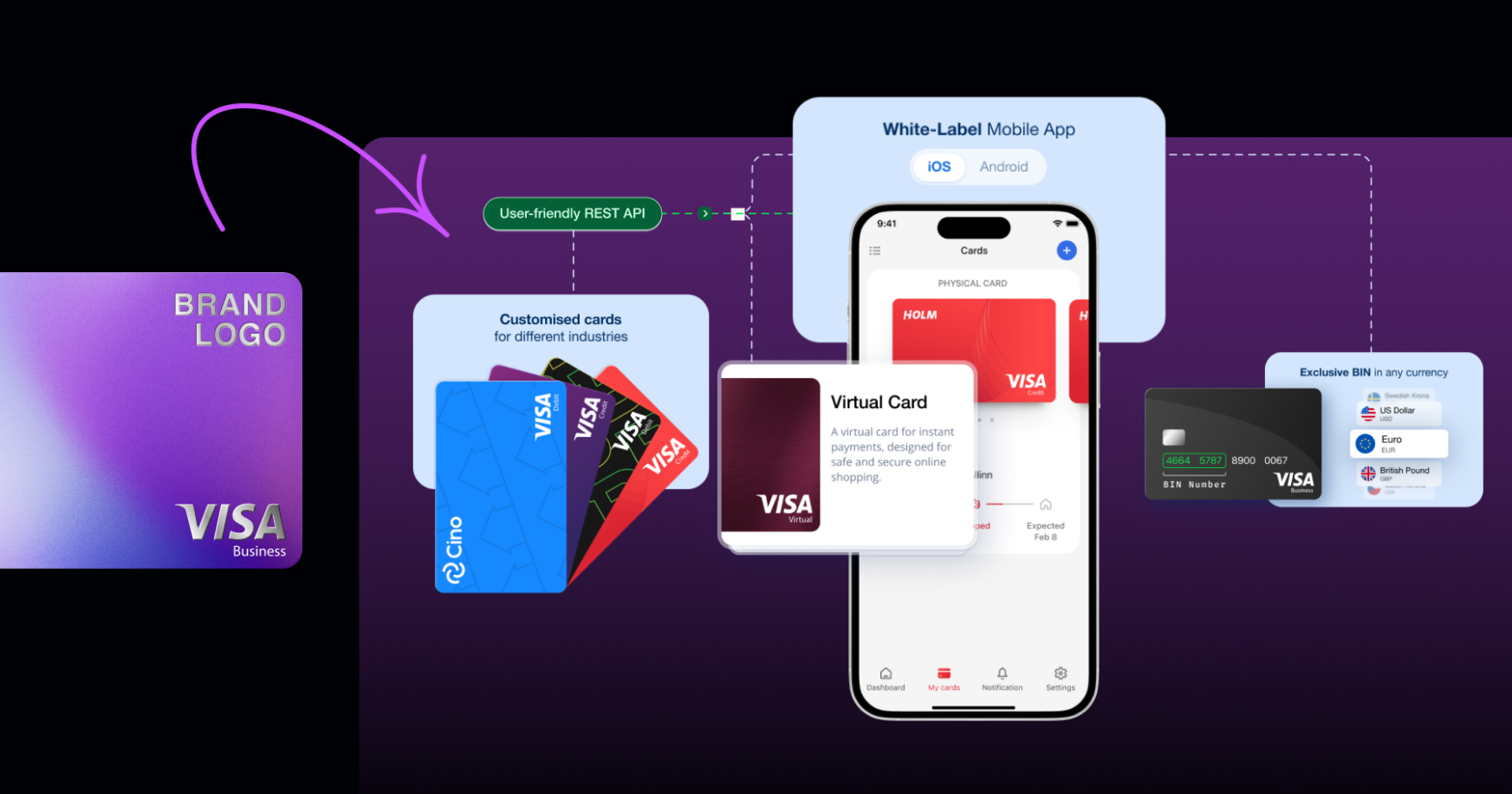

Wallester’s Role in the card ecosystem

Wallester is a licensed card-issuing institution based in Estonia and an official Principal Member of the Visa network. The company is authorised to issue all types of Visa-branded cards – debit, credit, prepaid, and virtual – for both individuals and businesses.

Wallester offers a full range of card issuing and processing services, including white-label solutions that allow organisations to launch their own card programmes without needing a direct licence from Visa. Wallester handles the entire infrastructure, from BIN sponsorship and card personalisation to transaction processing and compliance with KYC/AML regulations.

Built on a proprietary REST API platform, Wallester’s system allows businesses to integrate card issuing into their operations quickly and securely. The platform also supports direct integration with digital wallets like Apple Pay and Google Pay, providing full digital card functionality from the start.

Certified under the Visa Ready programme as a BIN sponsor and programme manager, Wallester meets the highest industry standards for security, reliability, and performance. By combining direct Visa network access with flexible technology, Wallester offers companies a practical and scalable way to manage card issuance, expense control, and customer payments across different markets.